Padel — A Hospitality Product Tested in Three Geographies

- Markus Gaebel

- 12 minutes ago

- 10 min read

Article 2 of 6 by Markus Gaebel, Racquet Sports Institute

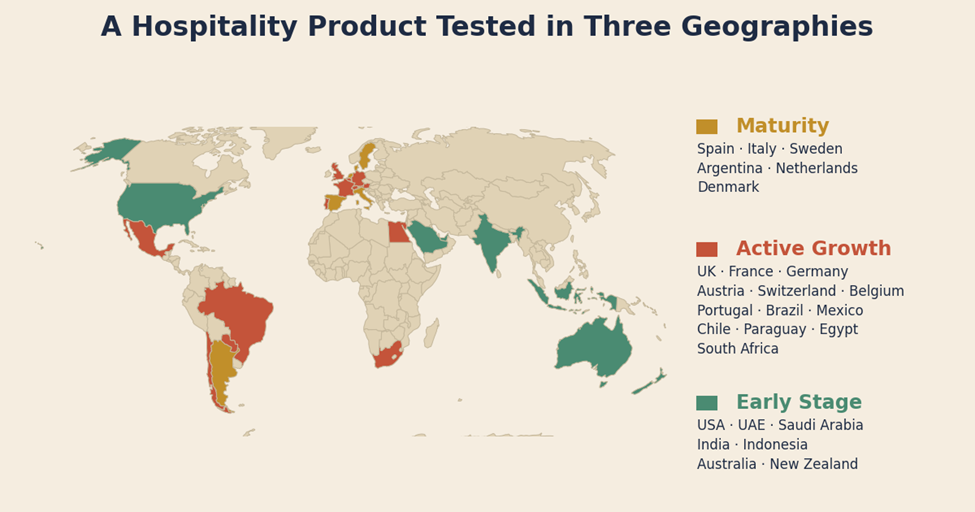

Padel is the same sport everywhere. Twenty by ten metres, four players inside glass walls, a beginner can rally within ten minutes. The business is not the same. Spain has approximately 17,300 courts and a mature, slowing growth curve. Italy has just crossed 10,000 courts and is consolidating. Sweden has lost many venues since 2022. The United Kingdom doubled its player base in a single year and now leads the world in gross monetary value per court. The United States and the Gulf are accelerating from a small base, India and Indonesia are early. The same court, four phases, five different business logics — and the investor who treats padel as a homogeneous global asset class misreads every market.

The padel player: who they are, why they play, how often

Padel’s commercial foundation is its player profile. Approximately 40 percent of players are women — the highest female participation rate in any racquet sport — with the average player aged between 25 and 45 (FIP World Padel Report 2025). In North America, the age distribution skews younger: 28 percent are 25–34, 31 percent are 35–44, 20 percent are 45–54, and only 9 percent are 55 or older (Rulo, North America 2025). The gender split in North America is reaching 45 percent female and increasing approximately 2 percent per year. Mixed doubles accounts for roughly 90 percent of all games played, which makes padel structurally the most gender-integrated racquet sport on the global market.

The frequency pyramid in padel is broadly consistent across racquet sports — approximately 3 percent fanatics playing more than twice a week, 15 percent enthusiasts playing once or twice a week, 30 percent recreational players playing more than once a month, and 52 percent casual dippers — but with two distinguishing features. First, the casual-to-engaged conversion rate is unusually high: the 92 percent retention rate after a first session means more casual dippers move into the recreational tier than in any other racquet sport (Playtomic / PwC, Global Padel Report 2025). Second, the doubles-only format means a single court hour generates four player-hours, which materially changes the demand-side mathematics relative to singles sports such as squash.

The motivational data on padel players is unambiguous and consistent across academic studies. Social connection is the dominant driver, ranking above competition, fitness, and skill mastery in nearly every sample (Burić et al., MDPI Sports 2025). Fun is the second strongest motivator. Health and fitness rank third. Competition becomes a meaningful driver only at higher skill levels — what researchers describe as the "maintenance phase" of participation, where players who initially came for the social experience develop competitive ambitions and league interest. Operators who understand this hierarchy build for connection first, fitness second, competition third. Operators who build a bare court complex — Sweden’s warehouse model — destroy the core product.

Sessions are typically 90 minutes. A padel court operating from 8 AM to 11 PM at strong utilisation delivers seven to eight bookable sessions per day. At full doubles, that produces 28 to 32 player-hours per court per day. Peak demand concentrates Monday-to-Friday between 6 PM and 10 PM and weekend mornings, accounting for roughly 40 percent of the weekly total — a concentration the operator must price and programme around.

Indoor versus outdoor: the Spanish lifestyle product meets the Northern climate

Padel originated as an outdoor sport in Spain, Argentina, and southern Mediterranean markets where year-round outdoor play is climatically viable. As the sport has expanded, the indoor share has risen rapidly because players in mature markets now prefer predictable conditions over outdoor lifestyle aesthetics. Italy passed 45 percent indoor inventory in 2025; the United Kingdom and Northern Europe are essentially indoor-only by necessity; Sweden’s expansion was overwhelmingly indoor-led. Spain remains the global outlier, with most courts still outdoor or covered rather than fully enclosed (Tennis Creative, 2026).

The capex difference is significant. An outdoor padel court runs approximately EUR 50,000 to 80,000 in court construction alone but minimal building shell — appropriate where land is cheap and climate supports year-round play. An indoor padel facility carries a building envelope at EUR 2.5 to 4 million for an eight-court footprint, which puts all-in capex per court at the EUR 450,000 to 550,000 range cited in Article 1. The indoor premium is justified by year-round utilisation and pricing power: indoor courts in mature European markets sustain 70 to 90 percent peak occupancy where outdoor equivalents collapse to 30 to 50 percent in the off-season.

The operator lesson is straightforward. Outside genuinely warm-climate markets — southern Spain, Italy, the Gulf, much of Latin America — outdoor padel works as a complement, not a primary product. The Sweden crash was in significant part an indoor-execution failure: too many cheap covered structures with poor lighting, poor acoustics, and no hospitality layer. The UK’s success has been the opposite: indoor-first, experience-led, modelled on Spanish premium clubs rather than Swedish warehouses.

Lens 1: The maturity zone — Spain, Italy, Sweden

Spain is the home of the sport and the global benchmark. With approximately 17,300 courts and 6.2 million players, padel courts now outnumber tennis courts by nearly three to one. Growth has slowed in line with what would be expected past the inflection point, and capital is shifting from greenfield development toward refurbishment and consolidation. This is not a failure of the market — it is what success looks like at the top of an S-curve (Tennis Creative, 2026; Statista, November 2025).

Italy is the second-largest padel market in the world, with 10,017 courts across 3,716 active clubs as of mid-2025. Forty-five percent of the inventory is now indoor, supporting year-round play and stronger unit economics. Growth has decelerated from 38 percent court additions in 2023 to 7–8 percent in 2024. The Italian padel sector now generates an estimated €1.5 billion in economic value. Two structural patterns define the consolidation phase: format polarisation — small neighbourhood clubs and premium multisport centres both thrive, while generic mid-tier Type 1 facilities are being squeezed out — and indoor primacy. Rome alone has 1,563 courts and approximately 250,000 players, the world’s third-largest padel city (Italia Team Padel, 2025).

The investor lesson from Italy is the most important nuance in the global padel market: consolidation is not contraction. It is the market separating professional operators from the speculative entrants of the 2021–2023 boom. The clubs surviving and growing built both businesses — leisure and real estate — with intent.

Sweden is the cautionary tale that should sit on every padel investor’s desk. Between 2019 and 2022, court count exploded from approximately 560 to over 4,200, reaching a density that exceeded even Spain’s. By 2023, demand normalised and the structural weaknesses became visible. Approximately 120 padel venues went bankrupt between 2022 and 2024. We Are Padel, the largest Nordic operator with 80 venues and over 600 courts, faced a monthly loss of approximately €1.4 million before restructuring. Total losses across the Swedish padel investment ecosystem are estimated at over €500 million (Branschaktuellt / Creditsafe, 2023).

The Swedish failure was not a failure of the sport. The operators who collapsed shared a common profile: capital-driven build-outs of basic warehouse structures with courts, in second-tier locations, at sub-scale court counts, with little or no investment in lighting, lounge, food and beverage, or programming. They treated padel as a real-estate yield play and ignored the leisure operation. When demand normalised, the leisure layer that should have retained customers did not exist.

Lens 2: The active-growth zone — United Kingdom, France

The United Kingdom is the most extraordinary growth story of any major racquet-sports market in 2025. The Lawn Tennis Association reports that 860,000 adults and juniors played padel at least once in 2025 — more than double the 400,000 figure from 2024 and a transformation from just 15,000 players in 2019. The country reached 1,553 courts across 559 venues, having hit the 1,000-court milestone a full year ahead of target. The Playtomic / PwC report ranks the UK as the global leader for highest gross monetary value per court, up 74 percent from 2023 (TrustPadel, 2026; Playtomic / PwC, 2025).

UK growth is not Sweden growth. Three structural differences explain the divergence. The LTA — the existing tennis governing body — has integrated padel into its organisational pathway. UK operators have concentrated on indoor or covered facilities. Capital deploying into UK padel has done so through experience-led venues with strong food and beverage, lounge design, and programming layers — modelled on Spanish premium clubs rather than Swedish warehouse builds. Many traditional UK tennis clubs have added two to four padel courts as a Type 4 member-retention tool, generating new revenue without cannibalising tennis. The result is rapid growth with sustainable per-court economics.

France is the largest single-market builder of new padel courts, with 1,272 added in 2024 — more than any other country in absolute terms. Over 150,000 FFT-licensed competitive padel players. Court additions are concentrated in southern France where climate supports outdoor primacy and in Paris where indoor venues anchor a maturing urban market. The French model is hybrid: a strong municipal-supported club network coexisting with growing commercial Type 1 venues (FFT via Padel Magazine, 2025).

Lens 3: The early-stage zone — USA, MENA, India, Indonesia

The United States is the most-watched market and the most genuinely early-stage. The State of Padel in the U.S. Report 2025 counted 112,872 active players and 688 courts across 180 facilities in 31 states as of Q2 2025. Over 50 percent of those courts had been installed since January 2024, and club growth was running at 51.5 percent year-on-year. Florida holds 41 percent of all U.S. courts, followed by Texas at 18 percent and California at 10 percent. Emerging chains include Padel Haus, Reserve, Bay Padel, Taktika, Ultra, Sense Padel, and Padel X (State of Padel U.S. Report 2025).

The U.S. capital story is the most institutionally underwritten in any padel market. The Pro Padel League closed a $15 million Series A in March 2026, following a $10 million seed round. Sunrise Padel Capital launched a $50 million Fund II targeting U.S. club development. North American real-estate developers committed nearly $200 million toward integrating padel courts into luxury residential and commercial projects between 2022 and 2024. Real acceleration is projected for 2027, with the U.S. expected to lead countries in total padel court count by that year.

The Middle East and North Africa is the most distinctive early-stage market because of its facility-type composition. Dubai alone has over 250 padel courts, a 60 percent growth over the previous two years. The UAE and Saudi Arabia together account for approximately 30 percent of all padel courts in Asia. New luxury hotel developments increasingly include padel courts as standard amenities alongside spa, gym, and tennis facilities. This is Type 5 (hospitality add-on) padel at scale, in a market where 78.5 percent average hotel occupancy and aggressive luxury development create a near-unique tailwind. The economics are less sensitive to per-hour court yield and more dependent on overall hotel performance (Arabian Business, March 2025).

India has gone from one court in Bangalore in 2017 to over 100 courts in 2024, with rapid expansion projected for 2025–2027. Mumbai alone has 50 to 60 courts, with operators including PadelPark, House of Padel, and Padel Rushh. Court rentals run ₹800 to ₹3,500 per hour, with cost-per-player at ₹200 to ₹900 when split among four players — a price point that has supported integration into luxury housing societies and gated communities. Indonesia registered the highest gross monetary value per court growth rate in the world in 2025 at +173 percent (Indian Padel Federation; Playtomic / PwC, 2025).

Reality check: 100 to 150 players per court applied to padel

Public padel statistics consistently report headline ratios of 300 to 400 players per court — figures based on the awareness pool divided by court count (FIP World Padel Report 2025). The operationally meaningful question is how those figures map onto the 100-to-150 active-players-per-court range that defines a viable commercial facility.

Spain at 6.2 million players against 17,300 courts produces a marketing ratio of 358 players per court. Apply the 18 percent fanatics-and-enthusiasts share and the operationally bookable demand drops to roughly 64 active players per court — already below the viable threshold, which is consistent with the slowing growth and consolidation visible in mature Spanish markets. Italy at 2.2 million players against 10,017 courts produces a marketing ratio of 220 and an operational figure of approximately 40 active players per court. Sweden at peak (~600,000 players against 4,200+ courts) produced an operational figure of approximately 26 — explaining why the warehouse model collapsed structurally rather than from any single bad operator decision. The UK at 860,000 players against 1,553 courts produces a marketing ratio of 554 and an operational figure of approximately 100 active players per court — squarely inside the viable range, which is why UK economics are currently the strongest in the global market. The United States at 112,872 active players against 688 courts produces an operational figure of approximately 30 active players per court — early-stage by definition, with capital betting on the catchment to deepen rather than on current demand to fill the courts.

The lesson is universal: in any padel market, halve the marketing ratio twice to get to the truth. The remaining number is what determines whether the business model works, and any business plan that uses headline figures rather than this operational reality is overstating projected demand by a factor of three to five.

Investment implications

In mature markets (Spain, Sweden), new development is hard. Strategic opportunities are refurbishment, brand consolidation, and acquisition of underperforming sub-scale operators by disciplined chains. In consolidation markets (Italy, Portugal, Belgium, Netherlands), the opportunity is selective new openings at proper scale and acquisition of distressed assets. In active-growth markets (UK, France), capital is deploying productively into experience-led venues at proper scale. The challenge is execution speed and securing premium urban locations. In early-stage markets (U.S., MENA, India, Indonesia), the capital window is wide. The risk is the same as Sweden’s — that less disciplined capital follows and builds sub-scale, operations-light facilities that fail when demand normalises.

Distressed asset opportunities — the second owner makes the money. A frequently underappreciated pattern in this sector is the systematic creation of distressed acquisition targets through bad management of fundamentally sound facilities. The Sweden crash, the Italian consolidation phase, and the residual sub-scale operations across Spain have all produced the same setup: facilities at the right scale, in the right locations, with sound underlying real estate, that have failed because the original operator built only the courts and ignored the leisure operation, the programming layer, the hospitality experience, or the financial discipline. These facilities often come back to market at a fraction of replacement cost — sometimes 30 to 50 percent of the original capex — because the original investors are forced to liquidate quickly and the asset alone, without an operator, has no obvious buyer at full value. The second owner, who arrives with operational competence and the capital to install the missing leisure layer, frequently makes the money that the first owner left on the table. This is one of the cleanest opportunistic theses in the racquet-sports sector globally and is currently most actively visible in Sweden and northern Italy, with secondary opportunities emerging in parts of Spain (Branschaktuellt / Creditsafe, 2023).

The next article examines pickleball through the same lens — a sport whose growth dynamics are dominated by a different facility-type architecture, a different generational tribe, and a different public-private tension that shapes every commercial decision in the market.

Comments