The Business of Racquet Sports: Why Most Investors Misread the Market — and How to Read It Right

- Markus Gaebel

- May 7

- 11 min read

Series introduction by Markus Gaebel — Racquet Sports Institute. Article 1 of 6.

Racquet sports are having their loudest decade in fifty years. Padel has reached 35 million players across 77,300 courts in 150 countries.[1] Pickleball has added more than 17 million participants in the United States alone in three years.[2] Tennis maintains 106 million participants worldwide.[3] Badminton has built a player base of more than 220 million globally.[4] Squash, the smallest of the five, still serves players in 185 nations.[5]

Yet the same decade has produced the largest concentration of Racquet-sports business failures since racquetball collapsed in the 1980s. Approximately 120 padel venues went bankrupt in Sweden between 2022 and 2024.[6] Squash participation in England fell by 27 percent for occasional players from pre-pandemic levels, on top of an estimated 40 percent decline over the prior decade.[7] In Munich — once home to an estimated 200 to 300 squash courts in the 1980s — most have disappeared.[8]

These two facts are not a contradiction. Racquet sports are a fast-growing global market with strong tailwinds, and a structurally unforgiving business that punishes operators and investors who do not understand what they are actually buying.

This series rests on a single analytical premise: Racquet-sports facilities are two businesses simultaneously — a leisure operation and a real-estate asset — and the people who win in this market are the ones who recognize that fact, plan for it, and run both businesses with professional discipline. This first article lays out the framework. The five that follow apply it sport by sport.

Five sports, five tribes, no cannibalization

A persistent narrative holds that the five major Racquet sports compete for the same player. The data does not support this. More than 75 percent of competitive-level players have sampled multiple Racquet disciplines, and cross-migration remains additive rather than substitutive.[9] The five sports serve five distinct customer prototypes.

Padel is the millennial third space — a 90-minute social game with bar, music, and an enclosed glass court that lets four players rally within ten minutes of trying it. Retention runs at 92 percent, gender split typically 60:40.[1] The product is connection.

Pickleball is the inter-generational bridge — the only Racquet sport where a 12-year-old, a 35-year-old, and a 70-year-old can play balanced doubles together. The product is democratic accessibility. [2]

Squash is the Gen-Z fitness instrument — 600 to 1,000 calories burned in 45 minutes, the smallest court footprint of any Racquet sport at roughly 62 square metres. Where the facility environment has been modernized, the sport thrives among urban professionals under 30; where it has not, it is losing ground.

Badminton is the institutionalized youth powerhouse — more than 220 million players globally, with deep integration into school curricula and public sports halls across Asia and parts of Europe.[4] Its mass-participation engine is publicly funded rather than privately marketed.

Tennis is the cross-generational classic — 106 million participants, the largest Racquet sport by absolute count, with a recreational core skewing 35 to 55 years old in Western markets.[3] The product is mastery, status, and tradition, currently being re-engineered through short formats and renovated club environments.

These five tribes meet the sport through five distinct facility types: commercial / for-profit (Type 1), public or non-profit / municipal (Type 2), school / college (Type 3), social member club (Type 4), and hospitality / hotel / workplace add-on (Type 5).[10] Which mix dominates a given region is the single most important variable in that market’s economics — and one this series returns to throughout. Egypt’s squash dominance, for instance, is not a sporting accident; it is the direct consequence of a Type 4 social member-club system that holds approximately 80 percent of the country’s player base.[11] Europe’s squash contraction reflects the opposite pattern: the grater majority of European courts are privately operated Type 1 facilities, the most exposed model in the current cycle.[12]

The two businesses: leisure operation plus real-estate asset

Every successful racquet-sports facility runs two businesses simultaneously. The first is a leisure operation: court hours, coaching, league play, food and beverage, retail, programming, atmosphere. The second is a real-estate asset: land, building, location, and the long-term appreciation curve of the property. Both businesses can succeed on their own terms — and frequently do — but they answer to different metrics and different time horizons. When their returns diverge sharply, the building eventually serves only one of them.

Mode A — Operator failure. The operator builds a leisure business and treats real estate as a passive container. This is the Sweden padel story. Between 2019 and 2022, court count exploded from approximately 560 to over 4,200, reaching a density that exceeded even Spain's.[6] When pandemic-era demand normalized, the operations-light, real-estate-light builds — sub-scale court counts, poor locations, no programming — could not absorb the correction. We Are Padel, the largest Nordic operator, faced a monthly loss of EUR 1.4 million before restructuring. Estimated total losses across the investment ecosystem exceeded EUR 500 million.[6]

Mode B — Owner-cashes in. The leisure operation runs profitably, sometimes for decades, while the underlying real estate appreciates faster than the operating yield can match. At some point the owner — entirely rationally — realizes the land's higher and better use and converts the facility. This is the Munich squash story: 200 to 300 courts in the 1980s, roughly ten centres in the entire metropolitan area today.[8] The operations were not failing; the owner simply captured a larger return by reallocating the asset.[13] For the owner, this is a successful exit. For the sport, the venue disappears all the same.

The structural insight that connects both failure modes: the two businesses must be run together, by aligned principals, with a conscious long-horizon strategy that prevents either side from cannibalizing the other. Owner-operator identity, long-term ground leases, member-club governance, or municipal ownership — what cannot work is two parties optimizing different metrics on the same building.

The investment reality: scale is sport-specific, but the scale logic is universal

The most common error in this market is opening a facility too small to absorb its fixed costs. The error is universal across all five sports, but the specific numbers that define "too small" differ sport by sport, and treating them as a single benchmark is itself a planning mistake.

All-in investment per court — including land, building shell, court construction, service areas, lighting, ventilation, technology, and proportional management overhead — varies by a factor of three or more across the five sports. A modern indoor padel court runs at approximately EUR 450,000 to 550,000 in mature European markets. A quash facility lands in a similar range. A standard indoor tennis court, with its substantially larger footprint, sits much higher per court when integrated into a multi-court facility.

hile premium Pickleball indoor commercial venues such as Picklr franchises sit closer to EUR 200,000 to 300,000 per court in European-equivalent terms.[14]

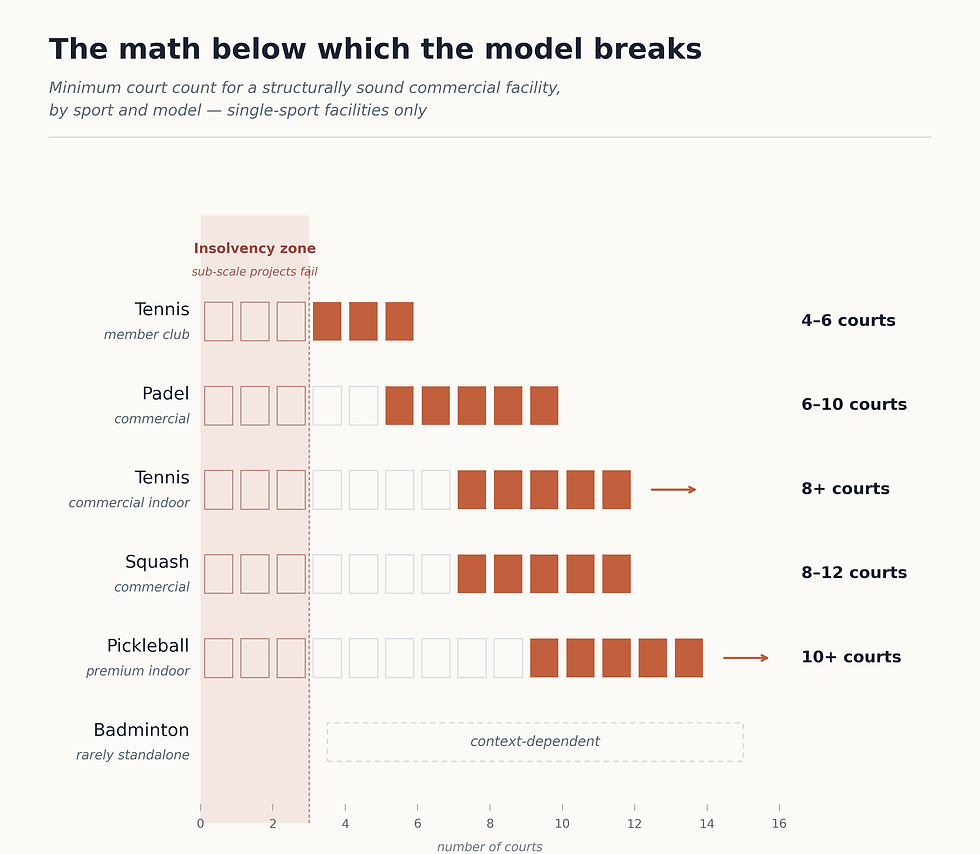

The scaling logic is the same across sports even though the absolute numbers differ. Where the threshold sits varies: padel typically at six to ten courts, with eight as a sweet spot; squash higher at eight to twelve plus a strong service layer, because per-session revenue density is lower; tennis depending on the model — a member-club configuration with four to six indoor courts can work, while a pure commercial indoor tennis operation typically requires eight or more; pickleball at ten or more for the Picklr-style commercial model that justifies a premium over public alternatives; badminton less about court count and more about whether the host facility absorbs the building cost.

Sub-scale projects fail with predictable regularity. Anyone entering a serious commercial Racquet-sports project with EUR 1 to 2 million is not building a facility. They are building an insolvency with a delivery date. The sector is littered with three- and four-court projects that launched on optimistic demand-side arithmetic, ran for a few seasons on enthusiasm, and quietly closed when the fixed-cost block proved immovable. This is not a failure of any sport. It is a failure of business planning that systematically underestimates minimum efficient scale.

The corollary is equally important: when these businesses are built at the right scale for the right sport, with both leisure and real-estate components actively managed, they are among the more attractive mid-cap real-asset investments available. Stable demand. Long product life cycles. High switching costs. Direct exposure to public-health, lifestyle, and demographic tailwinds. The economics work. They simply do not work at sub-scale.

The reality check: what 100 to 150 players per court actually means

The capex side of the planning equation is what most operators get wrong on the way in. The demand side is what they get wrong in year two, when the marketing-headline player numbers fail to translate into actual court bookings. Every published participation figure in this sector — the 35 million padel players, the 24.3 million American pickleball players, the 220 million badminton players — is a measure of awareness and casual exposure, not of bookable demand. The real calculation that determines whether a facility fills its courts is straightforward, and it is rarely communicated honestly.

Player populations in every Racquet sport follow a pyramid. Existing England Squash and Sport England analyses, used here as the master reference, distribute the active player base into four frequency tiers. Approximately 3 percent are fanatics who play more than twice a week — the league players, the competitors, the people for whom the sport is a primary identity. Approximately 15 percent are enthusiasts who play once or twice a week — the reliable members, the consistent court bookers. Approximately 30 percent are recreational players who play more than once a month but less than weekly — health-and-friends players, the social regulars. The remaining roughly 52 percent are casual dippers who play around once a month or less — try-out players, holiday users, the long tail of "I played squash once last year" responses that headline figures count as participants.[15]

Translating this pyramid into court demand produces the number that matters: a well-utilised commercial Racquet-sports facility runs on approximately 100 to 150 active players per court. That figure is consistent with Tennis Industry Association data (approximately 152 American players per court), with England Squash club benchmarks, and with Racquet Sports Institute facility-level analysis, which independently identifies more than 60 active members per court as the threshold for a viable programming layer.[14] Below 100 players per court, the facility cannot fill peak hours and cannot fund its programming. Above 150, peak-hour demand exceeds supply and players defect to competing facilities.

Compare this against the marketing-headline ratios that dominate the sector’s public discourse. The International Padel Federation reports approximately one court for every 400 amateur players globally.[1] USA Pickleball reports 24.3 million players against 82,613 courts — a ratio of 294 players per court.[2] These are not operational truths. They are the awareness pool divided by the court count, which is a useful indicator of growth potential and a misleading indicator of bookable demand. The fanatics-and-enthusiasts cohort that actually fills courts is closer to 18 percent of those numbers. Any business plan that uses headline participation figures to project court bookings is already wrong on page one.

Three additional mechanics shape how the 100-to-150 range plays out in practice. Session length: a squash court turns over up to twelve sessions per day at 45 minutes each, while a padel court typically is booked for 90 minutes. Players per session: padel and pickleball are doubles-only or doubles-dominant, generating four player-hours per court-hour, while squash is one-on-one. Peak-hour concentration: across all five sports, roughly 40 percent of weekly demand falls into Monday-to-Friday evening and weekend morning windows, which means the headline annual utilisation figure can mask collapsed off-peak performance. Each sport-specific article in this series quantifies these mechanics for the sport at hand.

Business of Racquet Sports divided into four stakeholders, one diagnostic toolkit

This series is not written exclusively for commercial operators. The Racquet-sports market is built on four distinct stakeholder perspectives, and each requires the same level of professional discipline.

The commercial operator seeks court-hour yield, ancillary spend, and asset appreciation. The Picklr franchise model in U.S. pickleball, Squash on Fire in Washington, and modern Type 1 padel chains in southern Europe represent the discipline this requires.

The government or municipality seeks mass participation and public-health outcomes — the UK’s Get Active strategy, Australia’s Sport 2030 framework, and China’s Healthy China 2030 plan all embed this objective at the highest policy level.[16] The Racquet-sports consequence is the rapid expansion of free or near-free municipal courts, most visibly in pickleball but increasingly in tennis park renovations and public badminton halls. This creates a structural pricing problem for commercial operators: a player who can use a clean public court for a few euros will not automatically pay forty for the same activity indoors. The commercial facility must therefore sell something the public park cannot — guaranteed climate, structured league play, professional coaching pathways, community.[17]

The non-profit or educational institution seeks social impact and talent pipeline. The Squash + Education Alliance operates 23 member programs across U.S. cities, enrolling more than 2,500 students with a 94 percent college matriculation rate; investment per facility runs USD 1–3 million leased, USD 4–12 million owned.[18] The College Squash Association governs intercollegiate squash across 65 varsity teams.[19] These are professional operations with multi-million-dollar capital plans.

The social member club seeks member retention, asset preservation, and identity continuity over decades. Heliopolis Sporting Club in Cairo holds over 42,000 family memberships and is one of the engines of Egyptian squash dominance.[11] Modern multi-sport conversions of traditional tennis clubs in the UK and Germany follow the same logic.

In all four cases, professionalism is the non-negotiable price of admission. The business model differs; the diagnostic discipline does not. A useful checklist of six basic questions applies regardless of stakeholder type:

Who is my customer? What generation, psychographic, catchment distance, price tolerance?

What is the facility-type ecosystem within a 15-minute radius of my site? Which Types are already serving which player tribes at which prices?

Have I sized demand against the 100-to-150-players-per-court reality, rather than against marketing-headline participation figures?

Have I cleared the minimum investment threshold for my sport? Court count, capex, and a margin of safety on fixed-cost absorption.

Am I running both businesses — leisure and real estate — with conscious alignment, or am I leaving one of them exposed?

What public or subsidized alternatives exist within my catchment? When present, adjacent municipal courts are the single biggest competitive threat to commercial Racquet-sports operations — and my pricing, programming, and service proposition must justify the premium over what is essentially free.

A facility that cannot answer these questions clearly is not yet ready to open. A facility that can answer them, and continues to answer them annually, has the strongest defense available against the structural traps this sector specializes in.

The market is real. The price of admission is professionalism.

Racquet sports are not a fad. They are a multi-decade structural growth story, driven by demographics that favor low-impact intensity, by public-health policy that subsidizes mass participation, by lifestyle preferences that reward social and game-based recreation, and by real-estate dynamics that increasingly value mixed-use leisure assets in dense urban catchments. The five sports do not compete with each other; they are five distinct products serving five distinct customer bases.

What the market punishes is the assumption that enthusiasm substitutes for analysis. The Sweden crash, the Munich disappearance, the UK decline, and the persistent failure of sub-scale builds are not warnings that the sector is unstable. They are warnings that the sector requires professional discipline. Facilities that have survived multiple decades share the same operating philosophy. They run two businesses on one balance sheet, at the right scale for their sport, with deliberate alignment of leisure and real-estate strategy, and with realistic demand assumptions grounded in 100-to-150 players per court rather than headline awareness figures.

The next five articles take this framework and apply it sport by sport. Each article goes deeper into the player profile of the sport in question — the frequency pyramid, the demographic and session mechanics, and the player motivations that determine what a facility must deliver. Each article also addresses the indoor-versus-outdoor question on its own terms, because that decision plays out very differently for badminton (almost exclusively indoor), squash (structurally indoor-only), tennis (predominantly outdoor in most markets, given the building cost of an indoor court of that footprint), padel (mixed, with strong indoor preference in mature markets), and pickleball (still outdoor-dominant in the U.S. but with a clear indoor commercial-premium model emerging).

The court is the stage. The show is everything else.

Sources

[2] Sports & Fitness Industry Association, 2026 Topline Participation Report; USA Pickleball court inventory data, 2025.

[11] SquashFacilities.com, The Secret Behind Egypt’s Squash Success, 2025; Heliopolis Sporting Club.

[13] Industry observation by Markus Gaebel, Racquet Sports Institute, on the Munich squash inventory (his hometown).

[15] England Squash, Understanding Player Types and Motivations, 2024; Sport England Active Lives Adult Survey 2021–22.

Comments