Pickleball — The Public-Sector Wave Meets the Commercial Operator

- Markus Gaebel

- May 14

- 9 min read

Article 3 of 6 by Markus Gaebel, Racquet Sports Institute

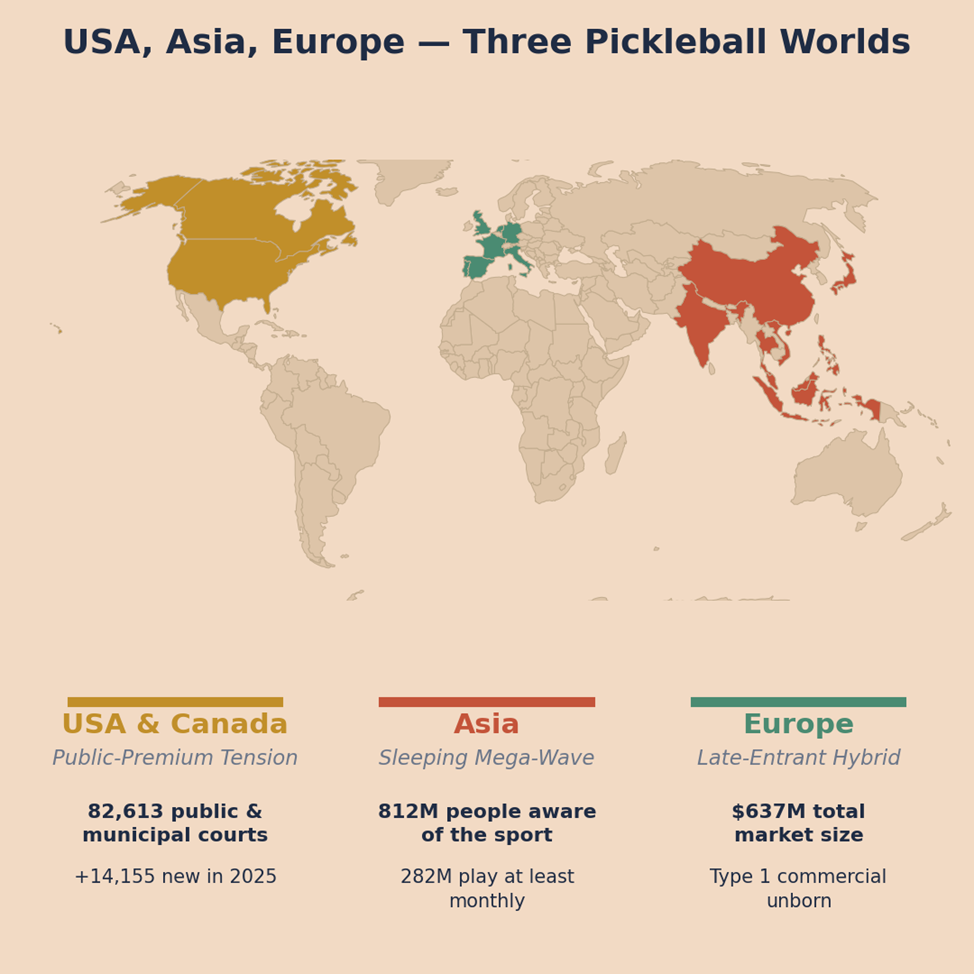

Pickleball is the racquet sport in which the public-private tension is most visible globally. In the United States, the country with the largest player base, the dominant story is the collision between an enormous wave of free or near-free municipal courts and a parallel wave of premium commercial operators trying to differentiate from "free." In Asia, the largest untapped market on earth, the dominant facility types are community grassroots courts and hospitality add-ons, with awareness running far ahead of built-out commercial infrastructure. In Europe, where pickleball arrived a decade later than in the US, the model is yet again different: tennis-club conversions and multi-purpose halls, with commercial Type 1 still essentially unborn.

Same paddle, same court, three radically different business stories.

The pickleball player: who they are, why they play, how often

The American pickleball player base in 2025 is 24.3 million people, of whom 7.48 million are core players (8 or more sessions per year) and 16.8 million are casual players (1 to 7 sessions per year) (SFIA Topline Participation 2026). The 25-to-34 age group is the single largest cohort at 16.7 percent of all players, with adults 65 and older accounting for 15.4 percent — pickleball is the only racquet sport with this dual-peak demographic. The average player age is 34.8, the gender split runs approximately 60 percent male and 40 percent female, and the household income skews above the national median (The Pickleball Era, 2025).

The pickleball distribution is approximately 3 percent fanatics (multiple sessions per week, league and tournament players), 15 percent enthusiasts (1–2 sessions per week, the SFIA core minus the most occasional core players), 30 percent recreational (multiple times per month, the deep core base), and 52 percent casual dippers (the SFIA "casual" category in full). The SFIA itself reports 31 days played per year on average among core players, down from 40 in 2022 — a decline driven entirely by the influx of new core players who have not yet built up their session count, not by existing players reducing engagement (SGB Media, 2023).

The motivational hierarchy in pickleball is the most empirically documented of any racquet sport. In a peer-reviewed survey of 3,012 participants using the Sport Motivation Scale, enjoyment scored 4.68 on a five-point Likert scale — the highest motivational score recorded across the racquet sports literature (Buzzelli et al., Sport Motivation Scale). Physical health scored 4.60, social connection scored highly across all age groups, and competition was a meaningful driver only among the most engaged "addicted" core players, who scored higher on competition and skill mastery than on social or fitness motivations (Frontiers in Psychology, 2025). For the 65-and-older cohort specifically, pickleball produces statistically significant improvements in life satisfaction, happiness, and reduction in depression and loneliness (Sage Geriatrics, 2025). The implication for operators is clear: programme for fun first, fitness second, mastery third, competition fourth — and the open-play "mixer" format, where winners advance and losers retreat, is the single highest-leverage product feature for retention.

Sessions are typically 60 to 90 minutes, with strong preference for open-play and round-robin formats over reserved court hours. Pickleball is doubles-dominant: a single court hour generates four player-hours, similar to padel. A pickleball court operating from 8 AM to 10 PM at strong utilisation can support eight to ten 90-minute sessions per day or twelve to fourteen 60-minute sessions, producing 32 to 56 player-hours per court per day — among the highest yields in racquet sports when programming is aggressive.

Indoor versus outdoor: the central economic question of U.S. pickleball

Pickleball is structurally the most indoor-versus-outdoor flexible of the five racquet sports. The court is small (13.4 by 6.1 metres), the equipment is light, and conversion of existing tennis courts, multi-purpose hardcourts, and even parking lots is cheap. The result is that the United States has built more than 82,000 outdoor or convertible pickleball courts at marginal cost, primarily through Type 2 municipal conversions (USA Pickleball, 2025).

This cheap-outdoor backbone is the central strategic problem for U.S. commercial operators. A player who can use a clean public outdoor court for free or for a few dollars will not pay $120 to $150 monthly membership for the same court access. The Picklr franchise model and its competitors — Pickleball Kingdom, Ace Pickleball Club, Dill Dinkers, Pickleland — have therefore built an explicitly indoor-premium product. Each Picklr facility runs eight to thirteen indoor courts in 25,000 to 60,000 square feet of converted big-box retail (former Bed Bath & Beyond, Big Lots, Rite Aid stores), with all-in startup costs of $850,000 to $2 million per location (Picklr, 2024–2026). What members are buying is not court access but the indoor experience layer: guaranteed climate, structured programming, professional coaching pathways, community, locker rooms, pro shop, food and beverage. The model works only if it is genuinely premium relative to the free outdoor alternative.

In Northern Europe and the Asian monsoon belt, the indoor-versus-outdoor question is largely settled by climate — outdoor pickleball is unviable for half the year. In MENA and South Asia, indoor and air-conditioned facilities have become the norm because outdoor summer play is impossible. Spain, Portugal, Italy, southern France, and the U.S. Sunbelt are the genuine indoor-versus-outdoor decision markets, where operators must explicitly engineer the differentiation rather than rely on climate to do it for them.

Lens 1: USA — the public-court wave meets sophisticated commercial capital

The American pickleball story is the most documented in the world and the only one where the public-private tension has reached structural maturity. The country has approximately 82,613 dedicated pickleball courts across 18,258 locations, and added 14,155 new courts in a single year — roughly 39 new courts every day. Florida alone hosts 1,071 pickleball locations, more than most countries have in total. The Racquet Sports Institute estimates a U.S. court shortage of approximately 24,000 courts and a financing need of approximately $855 million to close the gap (USA Pickleball, 2025; Racquet Sports Institute, 2025).

The commercial response is the franchise indoor club model. By the end of 2025, Picklr had over 80 locations open and more than 500 new clubs and 5,000 courts in active development, with 400+ franchise licenses signed in North America and international expansion under way into Canada and Japan (Picklr, 2024–2026). The collective pipeline across all major franchises represents one of the most aggressive commercial deployments in the racquet-sports sector globally. Geographic concentration is heaviest in the Sunbelt and Mountain West, with rapid Northeast and Midwest expansion driven by indoor-climate necessity.

The big-box retail conversion thesis deserves particular attention. Picklr and its competitors are reactivating dead suburban retail at industrial scale: a 30,000-square-foot vacant store becomes a 10-court facility, the leisure operation pays current rent, and the underlying real-estate asset benefits from the structural revaluation of underused suburban retail space. This is the Article 1 dual-business logic at industrial scale, and one of the more elegant alignments of leisure operation and real-estate strategy currently visible in the racquet-sports sector.

The risk on the U.S. commercial side is exactly the one Sweden’s padel market produced. Multiple franchises are racing into the same suburban catchments. Sub-scale or generic facilities will be the first to fail when the wave normalizes. The Picklr-class model works at proper scale (eight or more courts plus the experience layer); a four-court warehouse build will not.

Lens 2: Asia — the sleeping mega-wave

Asia is the largest untapped pickleball market on earth and has the most distinctive facility-type architecture of any region. The UPA Asia / YouGov 2025 study found that 812 million people in Asia have tried pickleball at least once, and 282 million play at least monthly. India alone counts 178 million people who have sampled the sport. Vietnam, Malaysia, and Indonesia are emerging as significant markets, with measurable acceleration in 2024 and 2025 (UPA Asia / YouGov, 2025).

These numbers reflect awareness and casual exposure rather than a built-out commercial ecosystem. The dominant facility types in Asia are community courts (Type 2), analogous to the public-park model that defined pickleball’s early U.S. growth, and increasingly Type 5 hospitality integrations in resorts, hotels, and luxury residential complexes. The pattern mirrors what we identified for padel in MENA and India: pickleball is finding its early commercial home as a hospitality amenity rather than a Type 1 commercial standalone.

The strategic implication for investors is the inverse of the U.S. picture. In the United States, commercial Type 1 capacity is racing the public-court wave and the customer is already paying for premium experiences. In Asia, the public-court wave is just beginning, there is no entrenched commercial infrastructure to compete with, and there is also no established player base habituated to commercial pricing. The first-mover advantage exists for operators who can build the full leisure-and-real-estate package in the right urban catchments, but the path to scale is longer than in the U.S.

Lens 3: Europe — the late entrant finds ready hosts

Europe is the late entrant. The European pickleball market reached approximately $637 million in 2025, with Germany leading at 5.9 percent of the global market, the United Kingdom at 4.6 percent, and France at 3.6 percent. Spain shows robust growth driven by expat communities and tourist resorts (Cognitive Market Research, 2025).

The European Pickleball Federation organized the second European Pickleball Championships in Rome in 2025, attracting athletes from 30 European nations. Spain topped the medal table, England finished second, Italy third — early indicators of where competitive depth is developing (European Pickleball Federation, 2025).

The European facility-type architecture is a hybrid of Type 4 (member-club add-on) and Type 2 (multi-purpose municipal halls). Tennis clubs across the United Kingdom, Germany, the Netherlands, and France are adding pickleball courts as a low-cost member-acquisition tool — a single tennis court can be repurposed into four pickleball courts with portable nets at minimal capex, generating new revenue without cannibalising tennis activity. Type 1 commercial pickleball is essentially unborn in continental Europe — there is no European Picklr equivalent at scale, and the climate and population-density patterns suggest the model would need to differ from the U.S. franchise pattern.

The strategic opportunity in Europe is therefore different from both the U.S. and Asia. The market is currently too small for aggressive Type 1 commercial deployment, but there is a meaningful Type 4 add-on channel for tennis clubs, padel clubs, and multi-sport venues seeking a low-capex, high-retention complementary product. The first European Picklr-style commercial chain — when it emerges, most likely in Germany or the United Kingdom in the 2026–2028 window — will face the same strategic question as U.S. operators: what value layers justify a premium over the free or low-cost public alternative?

Reality check: 100 to 150 players per court applied to pickleball

U.S. pickleball reports the most extreme marketing-versus-reality gap in any racquet sport. With 24.3 million players against 82,613 courts, the headline ratio is 294 players per court — far above the 100-to-150 viable range. But the operational reality is different and far healthier. The 7.48 million core players (8+ sessions per year) divided by 82,613 courts produces 91 active players per court — squarely inside the lower bound of the viable range. Apply the 18 percent fanatics-and-enthusiasts share to the full 24.3 million player base and the result is approximately 53 active players per court, indicating the U.S. court inventory is in fact roughly balanced against active demand at the national level (SFIA Topline Participation 2026; USA Pickleball, 2025).

The geographic distribution is what matters strategically. Florida concentrates 1,071 locations against a state population of 22 million, producing significantly higher per-court density of active demand than the national average. Sunbelt suburbs running at 150-plus active players per court are oversubscribed and represent the catchments where commercial Picklr-class facilities can charge premium memberships. Northern and Midwestern catchments running closer to 50 active players per court will support fewer commercial operators and more public-court complementary investment.

In Asia, the inverse picture: 812 million people have tried pickleball against an estimated 5,000 to 8,000 dedicated courts in the entire region. The active-players-per-court ratio is irrelevant because the supply is structurally too small relative to even the most conservative estimate of bookable demand. This is the rare market where the constraint is supply rather than demand, and where institutional capital deploying disciplined Type 1 and Type 5 capacity can capture meaningful first-mover position.

Investment implications

In the United States, the priority is execution speed at proper scale (eight or more courts plus the full experience layer) in catchments not yet saturated. The first-mover window in untapped suburban markets is closing as the major franchises race into the Sunbelt and now expand into the Northeast and Midwest. The big-box retail conversion thesis remains attractive given current cap rates on dead suburban retail.

In Asia, the priority is patient capital deployment in the highest-potential urban catchments — Indian metros, Vietnamese cities, Indonesian capitals, Singapore — with hospitality-led models that match local consumption patterns. The total addressable market is enormous; the addressable commercial customer is smaller and harder to reach.

In Europe, the priority is selective Type 4 add-on deployment through existing racquet-sports clubs and Type 5 hospitality integrations in tourism markets such as Spain, Portugal, and Italy. The first true Type 1 commercial chain will appear within two to three years; the bet is on which model, which operator, and which geography.

The next article examines squash through the same lens — a sport whose three-continent split tells the most extreme story in the racquet-sports sector of how facility-type architecture determines competitive outcomes both on and off the court.

Comments